filmov

tv

how to estimate exponential garch models

0:07:45

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch #egarch #igarch #cgarch #arch

0:10:25

GARCH Model : Time Series Talk

0:14:25

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

0:05:10

What are ARCH & GARCH Models

0:13:44

EGARCH model: exponential asymmetric volatility persistence (Excel)

0:21:30

GARCH model - Eviews

0:07:52

(EViews10): How to Estimate GARCH-in-Mean Models #garchmodels #garchm #tgarch #volatility #egarch

0:05:51

(EViews10): ARCH vs. GARCH Models (Estimations) #garch #arch #parsimony #volatility

0:01:11

How to Estimate an ARCH and a GARCH Model in Eviews (EN & GR Description)

0:22:22

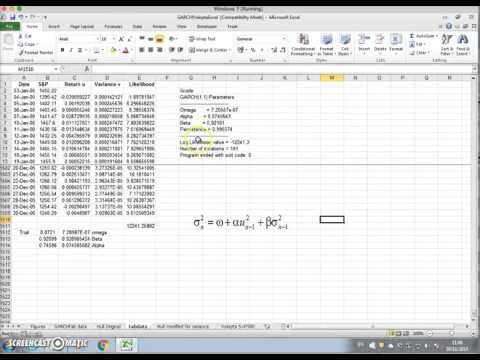

GARCH model - volatility persistence in time series (Excel)

0:08:13

(EViews10): Forecasting GARCH Volatility #forecast #garchforecasts #volatilityforecast

0:01:44

Exponential GARCH (EGARCH) Assignment Help

0:10:45

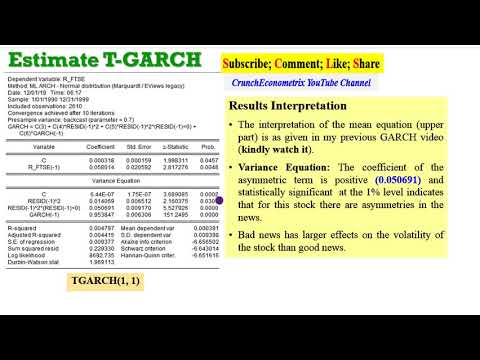

(EViews10): How to Estimate Threshold GARCH (GJR-GARCH) #garchm #tgarch #egarch #gjr-garch

0:06:07

10.3: EGARCH using RStudio

0:06:39

GARCH model estimated in Excel based on methodology developed by John C Hull using solver

0:10:08

Coding the GARCH Model : Time Series Talk

0:10:29

Time Series Talk : ARCH Model

0:11:12

ARCH and GARCH Models

0:18:42

GARCH model under non-normality: Laplace, Student, and error distributions (Excel)

0:11:34

GARCH Modelling for Volatility in Eviews

0:06:32

GARCH Volatility Model

0:15:49

EViews: (2 of 3) How to Estimate ARCH, GARCH, EGARCH & GJR-GARCH (or TGARCH) Models

0:08:01

EViews: (3 of 3) How to Estimate ARCH, GARCH, EGARCH & GJR-GARCH(or TGARCH) Models

0:09:33

G#4 EGARCH Model Introduction

Вперёд

join shbcf.ru

0:07:45

0:07:45

0:10:25

0:10:25

0:14:25

0:14:25

0:05:10

0:05:10

0:13:44

0:13:44

0:21:30

0:21:30

0:07:52

0:07:52

0:05:51

0:05:51

0:01:11

0:01:11

0:22:22

0:22:22

0:08:13

0:08:13

0:01:44

0:01:44

0:10:45

0:10:45

0:06:07

0:06:07

0:06:39

0:06:39

0:10:08

0:10:08

0:10:29

0:10:29

0:11:12

0:11:12

0:18:42

0:18:42

0:11:34

0:11:34

0:06:32

0:06:32

0:15:49

0:15:49

0:08:01

0:08:01

0:09:33

0:09:33